● Confidential UK Debt Help

Get debt help with an IVA

Leaving debts unpaid can often lead to bailiff action. Here’s how to prevent that

- Write off unaffordable debt*

- Lower your debt repayments

- Remove any worries or stress

To find out more about managing your money and getting free advice, visit Money Helper, an independent service set up to help people manage their money.

- Stop interest & charges soaring

- Lower your debt repayments

- Stop interest & charges soaring

- Write off unaffordable debt*

- Lower your debt repayments

- Remove any worries or stress

Write off unaffordable debt

Lower your debt repayments

Stop interest & charges soaring

To find out more about managing your money and getting free advice, visit Money Helper, an independent service set up to help people manage their money.

If you’re considering an IVA or other debt solution, you can also check if you qualify for help here ↓

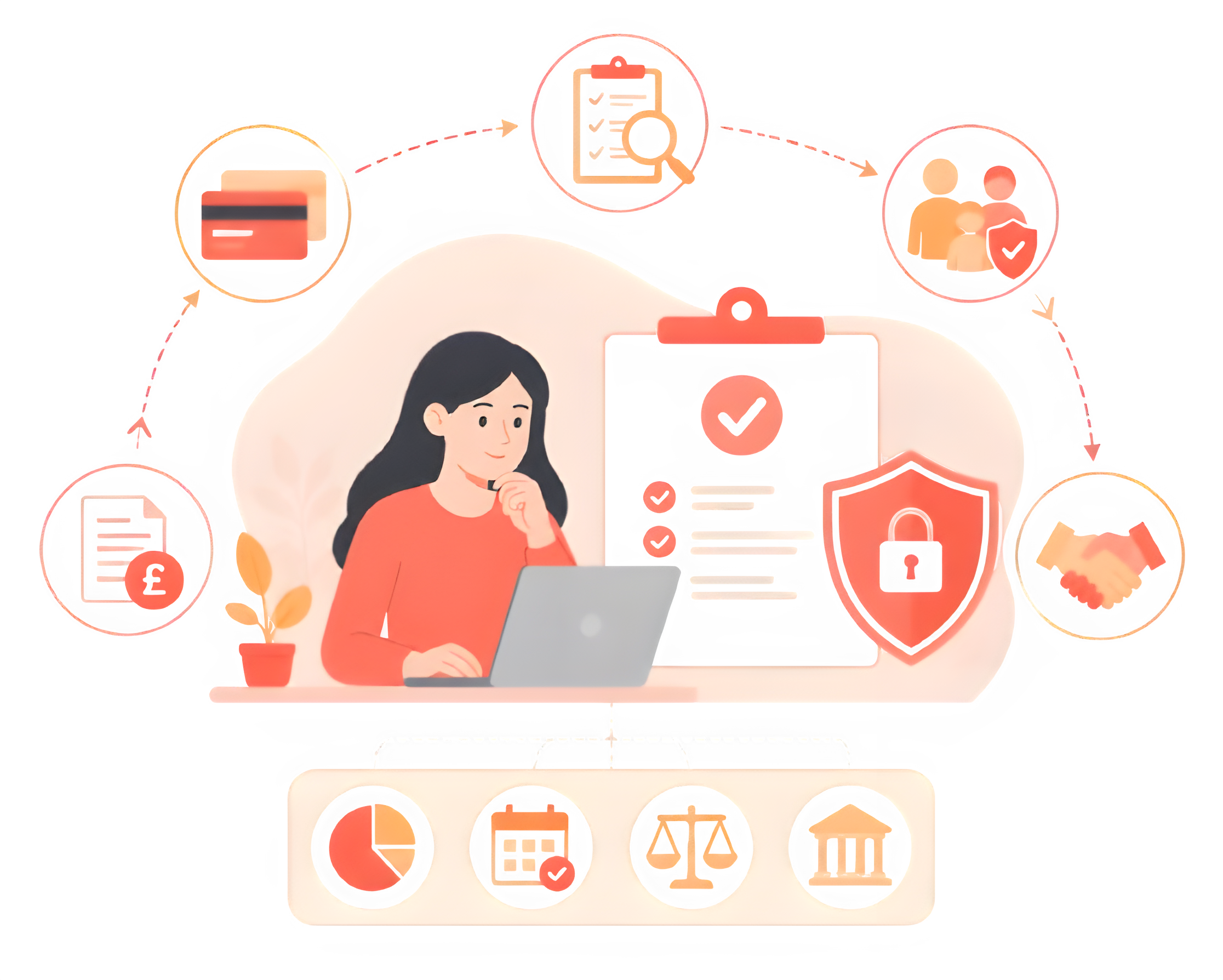

● What we cover

An IVA deals with all types of debt, including…

From high-street lenders to sub-prime loans, an IVA can reduce your repayments, write off unaffordable debt, and help you regain financial freedom.

Unsecured Loans

Credit & Store Cards

Utility & Catalogue Debt

Business Debt

Overdrafts

Complete the questions below and see if you qualify for help.

Safe, secure, confidential

Great news 🎉 it looks like we can help!

We just need a few more details to get your results.

Calculating your options…

One moment while we prepare your results.

● What we cover

An IVA deals with all types of debt, including…

From high-street lenders to sub-prime loans, an IVA can reduce your repayments, write off unaffordable debt, and help you regain financial freedom.

Unsecured Loans

Store Cards

Utility Bills

Business Debt

Catalogue

Overdrafts

● What to do

Achieving Debt Freedom, Starting with Just 3 Simple Steps

Getting out of debt can feel overwhelming but taking it one step at a time can lead you to complete financial freedom. Our process is simple, supportive, and tailored to your situation.

01

02

03

Take the First Step

Answer a few quick questions to give us a clear picture of your financial situation. This helps us understand how we can best support you.

Speak with Our Experts

Talking about debt can be difficult, but our empathetic experts will guide you through it.

Take Control of Your Debt

Once we’ve explored your options together, it’s over to you. With the right plan in place, debt freedom is within reach.

● What to do

Achieving Debt Freedom, Starting with Just 3 Simple Steps

Getting out of debt can feel overwhelming but taking it one step at a time can lead you to complete financial freedom. Our process is simple, supportive, and tailored to your situation.

01

02

03

Take the First Step

Answer a few quick questions to give us a clear picture of your financial situation. This helps us understand how we can best support you.

Speak with Our Experts

Talking about debt can be difficult, but our empathetic experts will guide you through it.

Take Control of Your Debt

Once we’ve explored your options together, it’s over to you. With the right plan in place, debt freedom is within reach.

● Check if you qualify

How IVA debt help works for you.

If you’re struggling with unaffordable debt, an Individual Voluntary Arrangement (IVA) could let you make one affordable payment, freeze interest and write off a portion of what you owe, whilst providing legal protection from creditors, including bailiffs.

● Why an IVA

Key benefits of an IVA

To find out more about managing your money and getting free advice, visit Money Helper, an independent service set up to help people manage their money.

Write off unaffordable debt

Potentially clear a significant portion of what you owe.

Lower monthly repayments

One manageable payment based on what you can afford.

Stop interest & charges

Frozen the moment your IVA is approved.

● Why an IVA

Key benefits of an IVA

To find out more about managing your money and getting free advice, visit Money Helper, an independent service set up to help people manage their money.

Write off unaffordable debt

Potentially clear a significant portion of what you owe.

Lower monthly repayments

One manageable payment based on what you can afford.

Stop interest & charges

Frozen the moment your IVA is approved.

Legal protection

Creditors can't pursue you or take further action.

Reduce stress & anxiety

Reclaim your peace of mind and your focus.

● Check if you qualify

When an IVA can help with debt

An IVA is designed for people with multiple unsecured debts (such as credit cards, loans and arrears) who can afford a reasonable monthly payment but not their current contractual payments. We’ll perform an initial fact find to see how best to help you. If you meet the criteria for an IVA you will be referred to our associate company Arkle Insolvency Limited for advice and information on the debt solutions available to you including a Debt Management Plan, Debt Relief Order or Bankruptcy so you can make a confident, informed choice.

● How it works

Achieving Debt Freedom, Starting with Just 3 Simple Steps

Getting out of debt can feel overwhelming but taking it one step at a time can lead you to complete financial freedom. Our process is simple, supportive, and tailored to your situation.

Take the First Step

Answer a few quick questions to give us a clear picture of your financial situation. This helps us understand how we can best support you.

02

Speak with Our Experts

Talking about debt can be difficult, but our empathetic experts will guide you through it.

03

Take Control of Your Debt

Once we’ve explored your options together, it’s over to you. With the right plan in place, debt freedom is within reach.

04

Struggling with unaffordable unsecured debt?

An Individual Voluntary Arrangement (IVA) could help you write off a portion of what you owe, reduce your monthly payments and give you legal protection from most creditors.

● The IVA difference

8 Ways Debt Help Could Benefit You

Professional IVA debt help can make a real difference, helping you regain control of your finances and reduce the stress of unaffordable debt.

1

Freeze interest and additional charges on your debts

2

3

Make just one affordable monthly payment

4

5

6

7

8

● Our process

Achieving Debt Freedom, Starting with Just 3 Simple Steps

Getting out of debt can feel overwhelming but taking it one step at a time can lead you to complete financial freedom. Our process is simple, supportive, and tailored to your situation.

1

Take the First Step

Answer a few quick questions to give us a clear picture of your financial situation. This helps us understand how we can best support you.

2

Speak with Our Experts

Talking about debt can be difficult, but our empathetic experts will guide you through it.

3

Take Control of Your Debt

Once we’ve explored your options together, it’s over to you. With the right plan in place, debt freedom is within reach.

Get In Touch Today

No long forms. No judgement. Just confidential, practical help — usually within the same working day.

- Free initial advice

- GDPR-compliant & confidential

- UK-based team

● IVA

Frequently Asked Questions

Everything you need to know about how an IVA works, who qualifies, and how it protects your financial future.

What is an IVA?

An Individual Voluntary Arrangement (IVA) is a legally binding agreement with your creditors to repay all or part of your debts over time, usually five years. Once complete, remaining qualifying debts can be written off.

Who can apply for an IVA?

How do I set up an IVA?

How long does an IVA last?

What debts can be included?

Will an IVA affect my credit score?

Yes. It stays on your credit file for six years from the start date and is listed on the Insolvency Register until three months after completion.